Circuits Split on Availability of ACA Exchange Subsidies

This morning, a three-judge panel from the U.S. Court of Appeals for the D.C. Circuit invalidated a 2012 IRS rule allowing tax subsidies in federal insurance exchanges under the Affordable Care Act. Within hours, a three-judge panel from the U.S. Court of Appeals for the Fourth Circuit issued a contrary ruling in a similar, but separate, case, allowing exchange subsidies in both state-based and federal exchanges. Though both decisions are still subject to further review and will have no immediate impact, such “circuit splits” are often considered strong evidence that a case will ultimately end up before the U.S. Supreme Court.

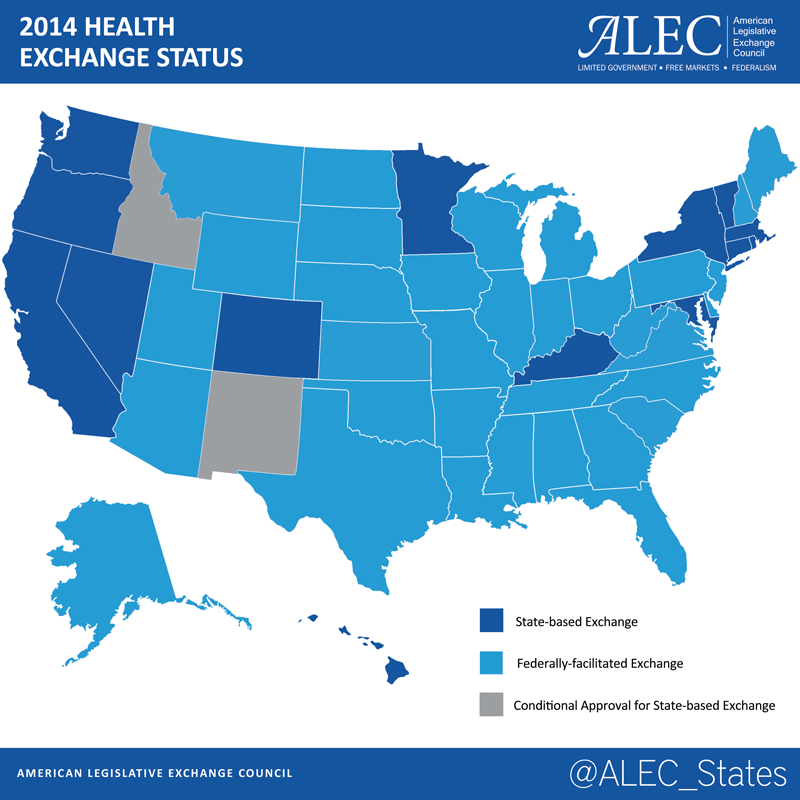

As has been covered previously in these and related cases, and before the ALEC HHS Task Force, at issue is whether the ACA’s subsidies for individuals to buy health insurance are available in states that declined to establish health insurance exchanges. Under the ACA, states were given the option to create state-based exchanges or default to a federal exchange—36 states chose to default, while just 14 currently operate their own (See map below).

The plain text of the ACA appears to provide subsidies only in exchanges established by the state. As has been noted previously, observers at the Kaiser Family Foundation acknowledged that the “claim that congress denied to the federal exchanges the power to distribute tax credits and subsidies seems correct as a literal reading of the most relevant provisions.” Additionally, the non-partisan Congressional Research Service previously noted that the law “seems to be straightforward on its face,” in making subsidies available only in state-based exchanges.

Nonetheless, in cases where statutory interpretation is in question, there is a strong legal precedent for judicial deference to agency interpretations of statutes, in this case the IRS. The result of this tension is what has been seen today in these two decisions. In a 2-1 ruling in Halbig v. Burwell, a D.C. Circuit panel held that the language of the ACA was clear in only allowing subsidies in state-based exchanges. In a unanimous ruling in King v. Burwell, a Fourth Circuit panel held that the language of the ACA was subject to multiple interpretations and deferred to the IRS.

The issues in both cases, however, extend beyond just the availability of subsidies.

Due to various mechanisms in the ACA, the IRS rule allowing for distribution of subsidies through federal exchanges also serves to trigger tax penalties on employers that don’t comply with the ACA’s employer mandate—the law’s requirement that businesses with 50 or more employees provide health insurance for employees or else face a fine. This circumstance arises because fines can only be imposed if an employer does not offer government approved coverage and an employee is eligible for tax credits through an exchange. If tax credits aren’t available, the employer mandate penalties would be effectively eliminated.

Similarly, because of the income thresholds ACA uses to calculate who is subject to the individual mandate, precluding the availability of subsidies would have the additional effect of exempting certain individuals from penalties for not purchasing health insurance.

States with attorneys general joining briefs in favor of striking down the IRS rule in Halbig include: Alabama, Georgia, Kansas, Michigan, Nebraska, Oklahoma, South Carolina, and West Virginia. Two similar cases, Pruitt v. Burwell, and Indiana v. IRS are still pending.