Krugman: Wrong on Taxes, Wrong on Kansas

New York Times columnist Paul Krugman recently used his weekly column to take aim at pro-growth tax reform and the Rich States, Poor States ALEC-Laffer State Economic Competitiveness Index. Krugman pulled no punches while dismissing the pro-growth impact of tax reform—Kansas’ recent tax reform specifically—seeing fit to call those he disagrees with “charlatans and cranks.” Issues of projection by Krugman aside, he is wrong on the economic evidence for tax reform and wrong on Kansas. His errors, omissions, and innuendo in the place of facts warrants correction.

First and most broadly, Krugman is wrong on the economic evidence analyzing whether taxes matter to economic performance. Dr. William McBride of the Tax Foundation has surveyed the academic evidence on taxes and growth and finds that more than 90 percent of peer-reviewed studies conclude that taxes do negatively impact economic growth, with taxes on personal and corporate income being the worst.

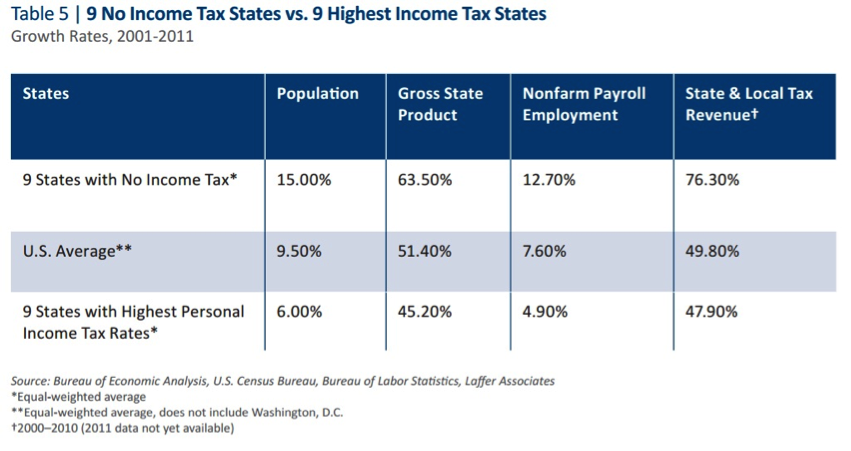

A simple review of the data demonstrates the same conclusion. Looking at the performance of the nine states with no income taxes versus the nine states with the highest income taxes, the performance results are fairly clear: no income tax states are vastly outperforming their high tax counterparts and the national average.

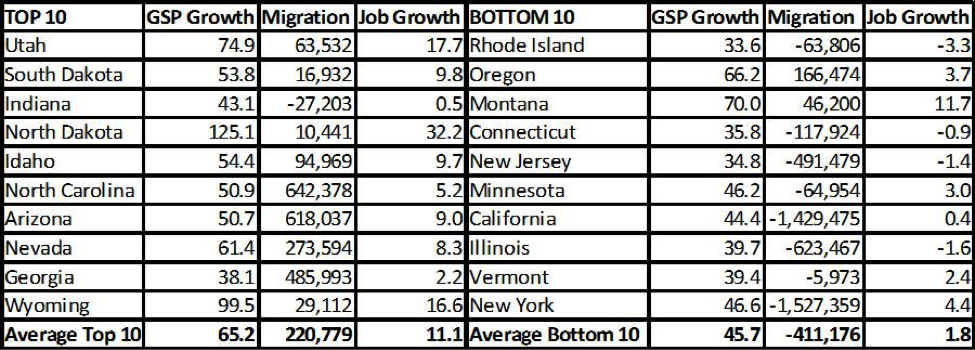

Moreover, as we have shown countless times, our own Rich States, Poor States ALEC-Laffer State Economic Competitiveness Index shows a strong relationship with state economic performance. First, a simple table displaying the economic vitality of the top and bottom 10 states in the index by looking at the last decade of performance in job growth, gross domestic product growth, and net migration of citizens. The results are stark: free states fair better than their big government counterparts.

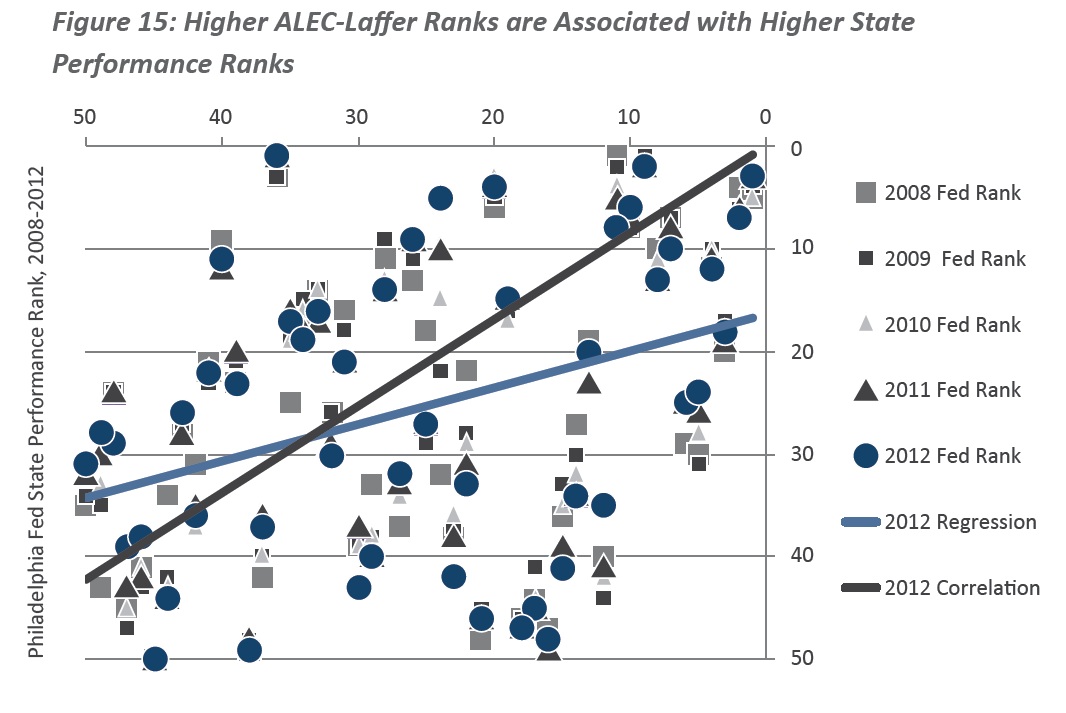

Second, more technical statistical research shows that economic freedom, as measured by Rich States, Poor States, is responsible for between 25 percent and 40 percent in the variation in state economic health, as measured by the index of the Philadelphia Federal Reserve Bank. Given the tremendous number of factors that affect differences in state economic health, this is a strong and significant result demonstrating clearly that public policy does matter to economic performance. The analysis comes from Dr. Randall Pozdena and Dr. Eric Fruits in their publication, Tax Myths Debunked.

Having established that taxes and economic freedom broadly do matter to economic growth, it is worth also considering Krugman’s claim about dynamic scoring—that small government tax reformers think “tax cuts pay for themselves.” Dynamic scoring of taxes looks at the likely revenue that would actually be lost or gained in a given tax rate change given the incentive effects of raising or lowering tax rates. Krugman says that small government tax reformers believes all tax cuts pay for themselves and, moreover, quotes right-of-center economist Greg Mankiw saying that the notion tax cuts pay for themselves is wrong. Ironically, ALEC recently published an essay on this very topic in the context of tax cuts in Nebraska and relied on the dynamic scoring estimates of none other than Greg Mankiw in claiming that proposed tax cuts wouldn’t decrease revenue as much as some expect, though stopping far short of claiming they would result in zero revenue loss. We can only assume Krugman didn’t do his homework in this regard or felt compelled to ignore the facts in order to make a cheap point.

Lastly, turning to Kansas, Krugman brings up three issues: lack-luster economic performance in the wake of tax cuts, an unexpected budget shortfall over projections, and a recent state debt downgrade by Moody’s credit rating agency. It’s worth discussing these issues one at a time.

Economic Performance: As Stephen Moore points out, Kansas’ tax cuts have been on the books for barely 18 months. If Krugman realistically believes that 18 months is the appropriate timeline to judge fundamental tax reform, he is the one guilty of “magical thinking,” not tax reformers. Moreover, the case that taxes do matter to economic performance has been extensively documented above.

Moreover, the lackluster economic performance Krugman notes has occurred under a mediocre policy regime characterized by the big government Krugman advocates (Kansas rated between 24th and 29th in Rich States, Poor States until 2013, when the state jumped to 11th), as the Kansas Policy Institute notes. During the past 10 years—before tax cuts—the state ranked 20th in state gross domestic product growth, 38th in net domestic migration, and 29th in non-farm payroll growth. Kansas is only now attempting to recover from bad policy. Will Upton of American for Tax Reform shows that Kansas’ economy has indeed improved since the tax cuts, particularly relative comparable states in the region.

Budget Shortfall: ALEC addressed this matter in a recent blog post and what was true then remains true now: the budget shortfall is largely not the result of Kansas’ recent tax cuts.

Lower than expected tax returns are largely the result of slow economy and federal tax policy. First quarter gross domestic product growth in the United States was an anemic 0.1 percent. Slow economic growth generally results in slow revenue growth, particularly for income tax collections. The Tax Foundation has recently pointed out that some of this may be the result of the expiration of bonus expensing, causing a notable fall investment early in 2014. This policy change, combined with a number of other federal tax and regulatory changes has created a difficult environment for economic growth in 2014.

Additionally, Joe Henchman of the Tax Foundation pointed out nearly a year ago that last year’s so-called “surge” in state income tax revenues was likely a one-time jump due to the federal capital gains rate jumping from 15 percent to 23.8 percent as part of the so-called “fiscal cliff” legislative compromises. As such, many investors accelerated their investment sales in order to avoid the increasing capital gains rates. This caused a spike in capital gain revenue last year and a sharp fall in capital gains revenue this year relative to trend. As Will Upton with Americans for Tax Reform has pointed out, the Congressional Budget Office also predicted this all the way back in January of 2013 for the same reasons.

Thus, the state’s recent revenue woes seem to have far more to do with what’s happening in Washington, DC, rather than Topeka, Kansas. Kansas State Department of Revenue has pointed out as much in their press release announcing revenue short-falls, although this has gone on deaf ears among those searching for an opportunity to assail Kansas’ pro-growth tax reform. As the press release and news reports across the country have noted, state tax revenue is down nation-wide, not just in Kansas. The Rockefeller Institute has documented as much in a recent data alert, noting personal income tax returns seem to be down nationally by 0.4 percent in the first quarter and in at least 10 different states. This includes states that didn’t take on any notable tax cuts in recent years. The Washington Post has also covered this dynamic.

The Kansas Policy Institute has further cleared up falsehoods and misconceptions on Kansas’ budget in a recent essay.

Debt Downgrade: From the same ALEC blog post on Kansas (which Krugman apparently did not read), we detailed the following on Kansas’ debt downgrade.

Turning to Kansas’ bond rating downgrade, Moody’s cited more than just recent tax cuts as the rationale for a downgrade, despite what opponents of tax reform are touting. Reliance on non-recurring revenues, a lack of spending cuts matching outlays to expected revenues, depletion of the rainy day fund, slow economic growth, and the underfunded state pension system were all noted as budget problems facing the state. That is to say that Kansas can improve their bond rating by addressing spending issues and boosting economic growth, not just raising taxes. Moody’s even makes clear in their analysis of Kansas that they do not view the lack of a state income tax as a source of credit risk. Standard & Poor’s has gone as far as to call low reliance on income taxes a boon to strong credit ratings, stating, “Sales tax-based revenue structure that exhibits sensitivity to economic cycles, but to a lesser degree than those of states that rely primarily on personal and corporate income taxes.”

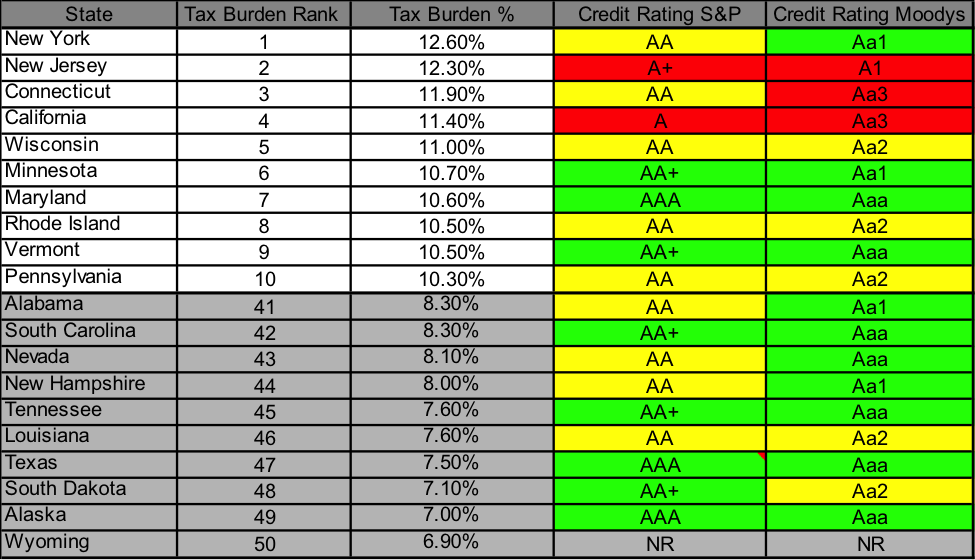

More broadly, is it true that states with high tax revenues have high bond ratings and states with low tax revenues have low bond ratings? The table below shows that this claim is false. The table compares the states with the 10 highest and lowest state and local tax burdens, according to the Tax Foundation, and lists their credit rating with Moody’s and Standard & Poors. States in the highest two credit rating category are in green, states in the third credit rating category are in yellow, and states in the fourth or lower credit rating category are in red.

States with lower tax revenues generally have higher credit rating and the states with the highest taxes in the nation generally have lower credit rankings.

In conclusion, not only is Krugman wrong on whether taxes matter to economic performance, he’s wrong on Kansas. Given this, it leaves us returning to the issue of projection: who are the real charlatans and cranks in this debate?