Tennessee Considers Eliminating Hall Tax

Tennessee policymakers are considering the repeal or “localization” of the Hall Tax, a tax on investment income (interest, dividends, and capital gains). The legislature is correct to consider this a pro-growth tax reform proposal. The Hall Tax, like all taxes on investment income, takes in little revenue while creating huge economic distortions and severely hampering economic growth. Repealing the Hall Tax is a pro-growth move that is sure to pay dividends in terms of job growth and income growth for all Tennessee citizens.

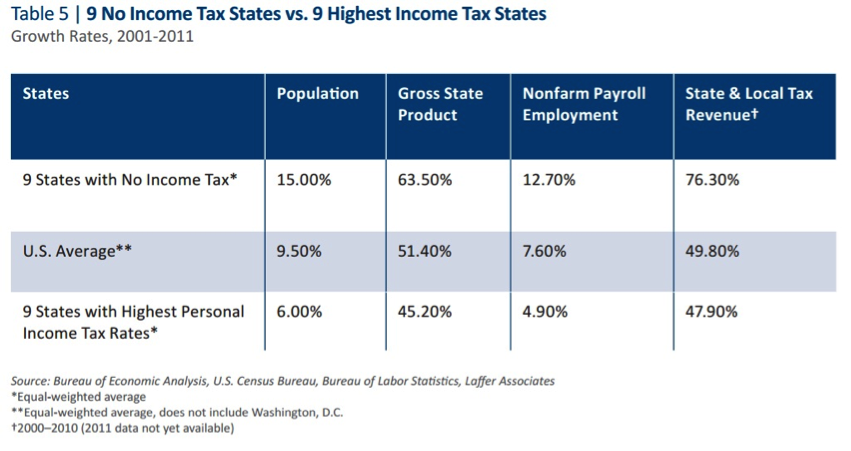

Tennessee is usually a state that tax-reformers hail as a role model, given that it has no taxes on wages or “pass-through” business income (businesses filling in the personal income tax code, instead of the corporate income tax code). Our frequently cited table that examines the performance of the 9 states without a state income tax versus the 9 highest states and the U.S. average, includes Tennessee as one of the 9 no income tax states:

But while Tennessee does not have a tax on wage or pass-through income, it does have a tax on investment income. That’s an unfortunate fact and a big asterisk for a state that otherwise has strong pro-growth tax policy.

Taxes on productive behavior, whether they are levied on wage income, business earnings, or investment income, reduce the incentive for these productive behaviors. The tax creates a “wedge” between the pure economic return of hard work, sound investment, and successful fulfillment of consumer demands, and how much reward an employee, business, or investor walks away with for their hard work. Since all income earners do their work in large part because they have the incentive to perform well and take away financial gain, lowering their gain through taxes means less incentives for productive behavior. Less productive behavior means a weaker economy that produces fewer things, creates fewer jobs, fails to grow personal income, and lowers citizen’s standard of living.

Since Tennessee clearly understands the economics of income taxation in terms of wage and small business income given the absence of a standard personal income tax; it’s worth pointing out that the same argument for an investment income tax applies here as well. Potential investors face a lower return on potential investments since taxes siphon off part of their return. As such, potential Tennessee investors have the incentive to either consume their income instead of invest, given the diminished possibility for a acceptable investment return after taxation eats up part of the gain, or simply take their investment dollars to a state that does not tax investment income, like Texas or Florida. Given that investment income provides for retirement security, higher wages through greater productivity of labor fostered by business investment, more funding for business start-ups, and increased innovation, lower levels of financial investment is a deeply harmful outcome for Tennessee’s citizens and harms the state’s economic competitiveness.

This is not just theory and conjecture: the totality of economic evidence on the connection between taxes and growth bear this out, showing that taxes on various forms of income (wage, business, and investment) harm economic growth more severely than any other tax. Tax Foundation’s Chief Economist has pointed out in two papers (one and two) that roughly 90 percent of all of the economic studies ever conducted conclude that taxes hurt economic growth, income taxes in particular.

The harmful economic effects of investment income taxes is precisely why the representatives of the states at the American Legislative Exchange Council have passed model policy on the elimination of investment taxes, as well as a resolution on the principles of sound tax policy. Needless to say, a tax on investment income violates a number of the core principles of sound tax policy and as such, is a tax that should be avoided by states.

Thankfully, the Tennessee legislature is considering reform proposals that would phase out and eliminate the Hall Tax. This is the right choice for economic growth and would have a negligible impact on the Tennessee government’s ability to provide public services. As Scott Drenkard of the Tax Foundation has pointed out, the Hall Tax only represents 0.9 percent of the Tennessee’s state and local revenue. Specifically concerning the revenue picture for localities, Drenkard notes that over 90% of cities have collected less than five percent of their revenue from Hall tax distributions. Moreover, every county in Tennessee takes in less than 0.5 percent of total revenue from the Hall Tax.

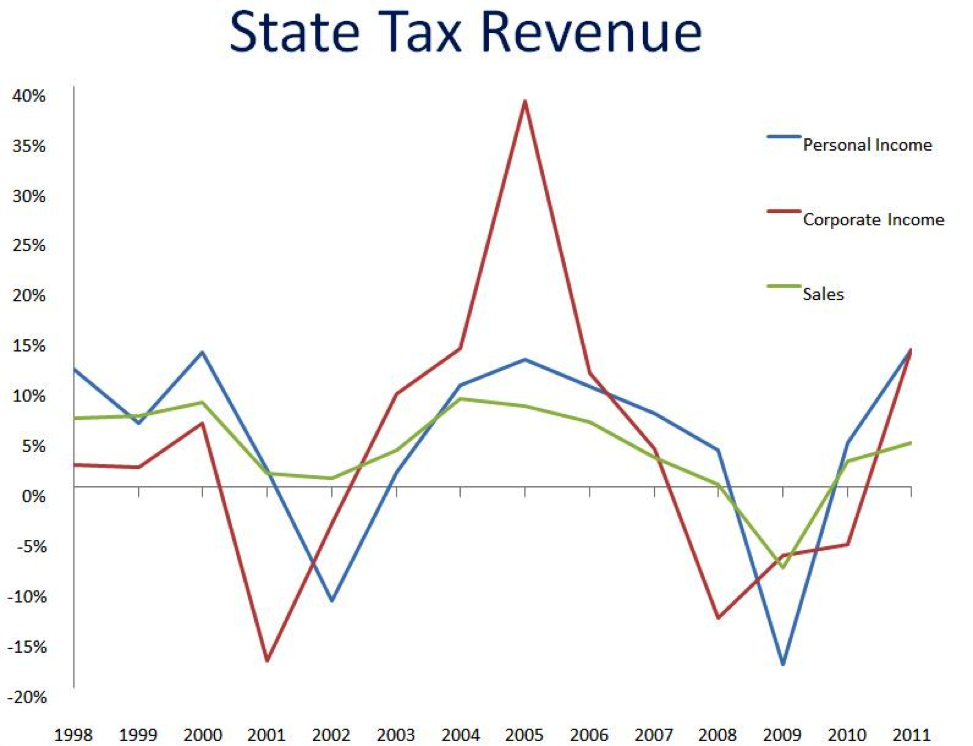

Given the low levels of revenue the tax takes in, Tennessee policymakers can have their cake and eat it too: they can improve Tennessee’s economic competitiveness and economic performance, while avoiding a large budget hole in the state and local ledgers. They are also moving away from an extremely volatile revenue source. As the chart below shows, taxes on income fluctuate more than any other revenue source. Moreover, since investment return fluctuate even more than traditional wage income, an investment income tax, like the Hall Tax, is likely on of the most volatile a state could possibly impose.

In short, Tennessee is quite right to look to eliminate a tax that hurts growth of income and jobs, distorts incentives, pushes investors out of state, doesn’t take in much revenue, and experiences extremely volatile revenue collections. The economic gains and growth dividends that the Volunteer State can realize by not taxing investment gains and financial dividends are significant. This is why national groups like Americans for Tax Reform and the Tax Foundation, along with state groups like the Beacon Center of Tennessee, have said positive things about the Hall Taxes phase-out or repeal. Easing or eliminating the burden of the Hall Tax is a huge step towards improving Tennessee’s economic policy environment. This will enable growth in broadly shared prosperity and the ability of citizens to achieve the dignity of work, financial success, and entrepreneurial venture.