On Saint Patrick’s Day, U.S. Has Much to Learn From Ireland

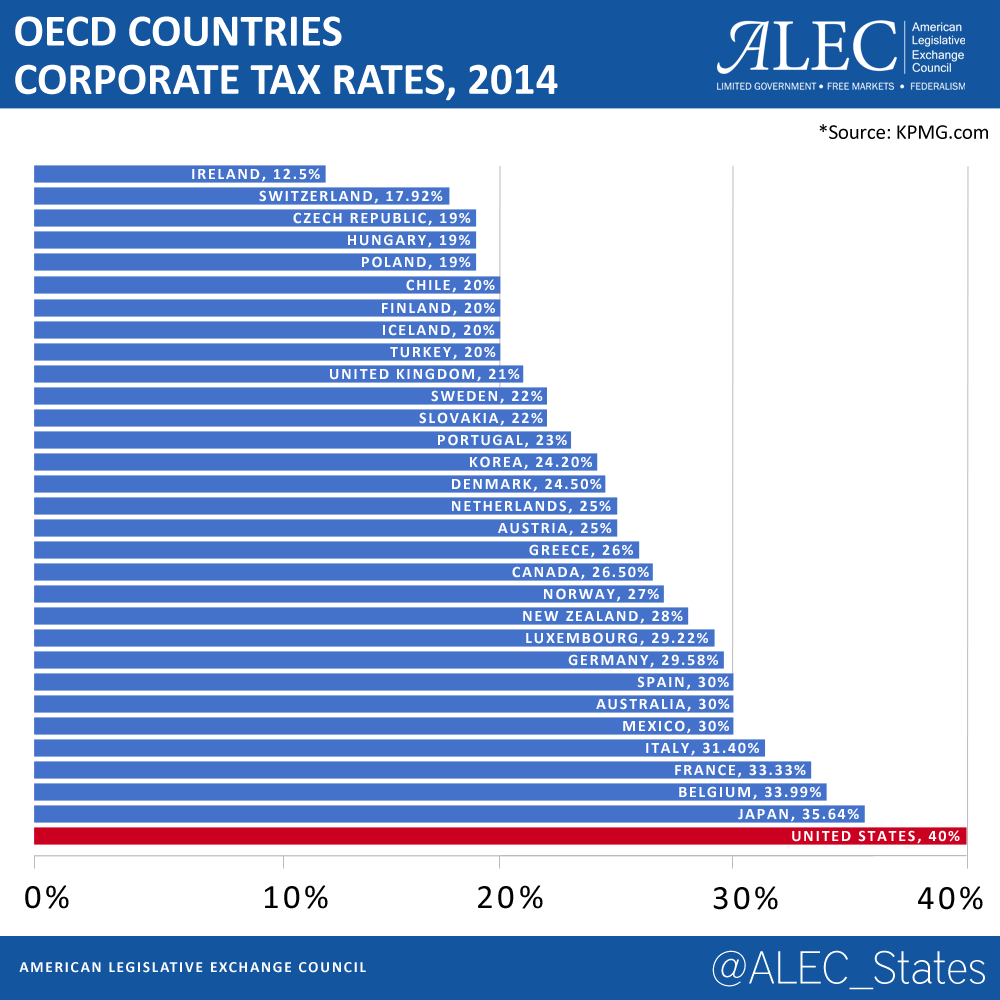

While Saint Patrick’s Day gives people all over the world a reason to be Irish for a day, it might be better for the United States to move permanently ‘Irish’ when it comes to corporate income tax rates. The United States currently has the highest corporate income tax rate in the developed world at 35 percent federally, and reaches almost 40 percent once the average state corporate income tax rate is included. By contrast, Ireland maintains a top statutory rate of just 12.5 percent, less than a third of the top U.S. rate. This competitive, pro-growth corporate income tax rate has certainly paid off. Ireland’s economy struggled during the past few years, due mainly to an economically depressed Eurozone that reduced demand for Irish exports, but is now making a come-back. Ireland experienced 7.7 percent growth in Gross Domestic Product (GDP) during the second quarter of 2014 from the second quarter of 2013. This high growth rate was achieved while the Eurozone as a whole saw little or no growth in GDP. These figures have led some to estimate that the Irish economy could grow by as high as 5 percent in 2014.

Meanwhile, in addition to maintaining an uncompetitive corporate income tax rate, the United States is also one of only 7 of the 34 Organisation for Economic Co-operation and Development (OECD) countries still operating on a worldwide corporate income tax structure. This means if a U.S.-based company makes a profit anywhere in the world and wants to bring that profit back to the U.S., the profit is taxed at the highest corporate income tax rate in the world (with a credit for any taxes paid to a foreign government where the income was earned). The U.S. corporate tax system stands in stark contrast to a territorial corporate income tax system, which only taxes companies on profits earned in the country, rather than taxing the total global profits of companies.

In an increasingly globalized economy in which capital and labor is more mobile than ever, it should not be surprising that the low corporate income tax jurisdiction of Ireland is an attractive place for companies to do business. Many U.S. companies do business in Ireland through subsidiaries and contribute to its economy rather than declaring that income in the United States. In fact, some of Ireland’s largest corporations are U.S. subsidiaries, owned by companies like Microsoft and Oracle.

The United States corporate income tax rate is becoming increasingly cost prohibitive to pay when other countries rates are much more competitive. This competitive corporate income tax system is not unique to Ireland, although Ireland is certainly one of the most competitive. The United Kingdom only levies a 21 percent corporate income tax and Canada only levies a combined federal and provincial rate of 26.5 percent; both countries also operate on a territorial corporate income tax system rather than a worldwide corporate income tax system.

It is well established that taxes negatively impact economic growth. Research from Rich States, Poor States: ALEC-Laffer Economic Competitiveness Index highlights the effects of corporate income taxes on the state level. From 2003 to 2013 the eight states with the lowest corporate income taxes experienced growth in jobs of 12.1 percent, more than double the 5.1 percent job growth from the eight states with the highest corporate income taxes. This trend of the eight states with the lowest corporate income taxes outperforming the eight states with the highest corporate income taxes continues in the areas of domestic migration, gross state product growth and personal income growth. Internationally, the impact of high corporate income taxes is also taking its toll on the U.S. economy. From 2000 to 2011 alone, the U.S. saw a net loss of 46 of the Fortune Global 500 company headquarters.

There is no reason to think this trend will improve anytime soon. From 1997 to 2011, 30 of the 34 countries in the OECD reduced their corporate income taxes; the U.S. was one of just four countries not to lower corporate income taxes during this period. Even if the U.S. does not follow the Irish to a competitive 12.5 percent corporate income tax rate, there is a clear need for reform.

Canada reduced its corporate income tax rate to just 15 percent (federally) from 28 in the 1990s and it collects more revenue now as a percentage of GDP than it did when the rate was substantially higher. In fact, Canada now collects about 1.9 percent of GDP through its 15 percent federal corporate income tax. The United States collects about 1.8 percent of GDP through its 35 percent federal corporate income tax. Lowering tax rates and removing carve-outs and loopholes is a way to simplify the convoluted U.S. corporate tax structure and work to reverse the economic damage done by maintaining the world’s highest corporate income tax rate.

When thinking about Saint Patrick’s Day and everything Ireland has to offer, the Irish model of a more competitive, pro-growth corporate income tax is among its greatest economic features.