William Freeland Testimony on Illinois Tax Competitiveness

On January 17, 2014 Research Analyst William Freeland testified at the Illinois General Assembly Committee Hearing on State Competitiveness and Tax Teform. His written testimony can be found below,

My name is William Freeland and I’m a research analyst with the American Legislative Exchange Council’s Center for State Fiscal Reform. The American Legislative Exchange Council works to advance the fundamental principles of free-market enterprise, limited government, and federalism at the state level through a nonpartisan public-private partnership of America’s state legislators, members of the private sector and the general public. ALEC proudly calls nearly a third of all state legislators its members. ALEC was founded in 1973 in Chicago so I’m proud to speak to you today in our organization’s birthplace.

I’ve been asked by the committee staff to share ALEC’s research on state economic competitiveness, particularly with respect to tax reform. I’m pleased to share ALEC’s research and I commend the Illinois legislature’s inquiry into improving the state’s public policy environment. As a Midwest native coming from Michigan, Illinois and Chicago in particular have always had a special place in my heart. I hope today’s dialogue can lead to the adoption of policies that improve the wellbeing of this great state’s citizens.

I’d like to begin by sharing the results of ALEC’s annual state competitiveness ranking index, Rich States, Poor States. Now in its 6th edition, Rich States, Poor States ranks all 50 states on both economic performance over the last decade and the state’s “economic outlook,” or prospects for future economic performance. The study is authored by Jonathan Williams, tax and fiscal policy director of ALEC; Steve Moore, senior economics correspondent for the Wall Street Journal; and Dr. Arthur Laffer, famed economist and developer of the Laffer curve. The study ranks economic performance based 3 criteria, equally weighted over the last decade: state gross domestic product growth, net domestic migration, and payroll employment growth. The study ranks economic outlook based on 15 equally weighted variables, including measures of taxes, regulatory policy, labor policy, debt, and other important policy variables. These 15 variables give a picture of the relative economic freedom of a state and have been found to strongly correlated to the economic health of a state [1].

Rich States, Poor States ranks Illinois 47th on economic performance and 48th on economic outlook. Illinois has ranked in the bottom 10 states in economic outlook in every one of the publication’s six editions. The fact that Illinois ranks 47th in economic performance and 48th in economic outlook is no coincidence. Economic policy has a real effect on economic outcomes. Economic freedom translates in to a policy environment that facilitates broadly shared wage growth, mobility of labor up the earning ladder, entrepreneurship, and the attraction of talented people, successful businesses, and capital investment to a state. Though I’m an economist by trade and these assertions are based on data, economic theory, and statistical studies, the real world effects of strong economic performance should be understood in human terms. Widely shared economic prosperity empowers citizens to achieve the America dream and puts them in the driver seat of their economic destiny. Many decisions—whether to marry, have kids, which state to locate in, whether to start a business—are strongly tied to economic realities citizens face. In short, economic freedom leads to economic prosperity which leads to individual empowerment and the dignity of human achievement.

With this in mind, I’d like to share some key areas that Illinois can improve in order to boost the state’s economic potential. The most significant area is likely in tax policy. First, to focus on a positive, I’d like to discuss Illinois income tax. While the state does not have the most competitive income tax in the country, it rates at 17th for the top marginal rate and 14 for progressivity. The rate is roughly in the middle of the pack at 5 percent, but the fact that the state does have a flat tax is an asset.

Economists find that while all taxes are correlated with economic performance, personal and corporate income taxes are most strongly correlated [2]. This is because income taxes are levied on productive behavior: wages come from hours engaging in productive work, business profits from successfully serving customers, and capital gains from sound investment decisions. Since income taxes lower the real return on these activities, economists view them as lowering the incentive to engage in productive behavior. What this means is that people are less willing to go to the trouble engaging in work over leisure or taking the risk of investment over income consumption, the more they are taxed. This lowers economic activity and harms economic growth.

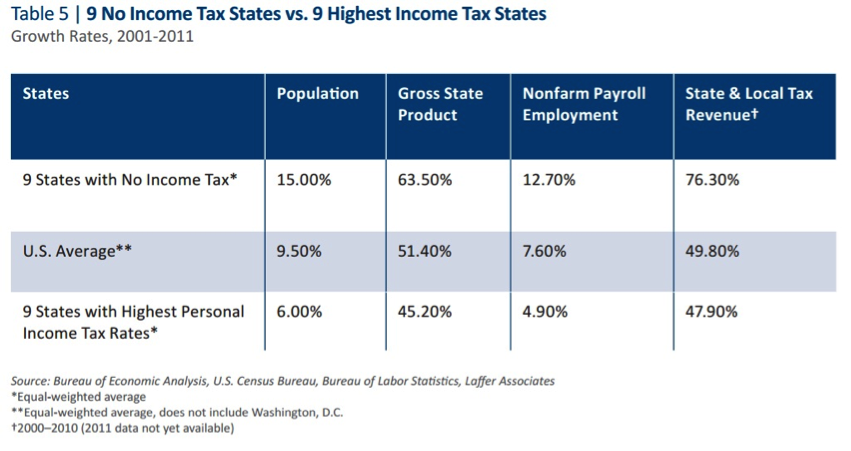

Given this, taxes on income—both personal and corporate—should be low as possible to maximize growth. Instead of raising income tax rates, allowing temporary tax increases to become permanent, or making the states flat tax into a graduated or progressive income tax, the state would be best served by lowering the personal and corporate income tax burden. Not only is the personal income tax in the middle of the pack in terms of state rankings, the corporate income tax ranks near the bottom at 44th. Lowering these taxes, while lowering the overall burden of taxation as well, would have a tremendous impact on economic performance. I’ve included a chart in my written remarks which can also be found on page 39 of the most recent edition of Rich States, Poor States. It compares the economic performance of the 9 states with no personal income tax to the 9 states with the highest personal income tax. As you can see, the states with no personal income tax greatly outperform the states with a high personal income tax over the last decade. Turning to more sophisticated economic research, the vast majority of studies find that higher personal income tax rates and corporate income tax rates hurt economic growth [3].

In terms of paying for cuts to the state personal and corporate income tax, I suggest two primary means. First, look to lower spending by reducing the scale of government to core competencies that only government can provide and are absolutely necessary to unlock economic prosperity. This goes beyond eliminating waste, fraud, and abuse in the budget, and taking a good hard look at what Illinois must do for it citizens and what services are not worth the trade-offs of an uncompetitive policy environment. After all, the greatest service Illinois can provide for its citizens is a job in the private sector and a growing wage. Though many public investments do help unlock economic growth, the economic concept of diminishing margin returns is relevant here. The more that Illinois spends on various strategic investments, the lower the growth premium return of those investments. Relative to the growth premium and corresponding impact of human well being of tax cuts, the impact of additional dollars of public spending is likely far smaller. Illinois would be better served by setting aside the prospect of additional public investment and instead look to make government lean and focus on providing the core functions of government as efficiently as possible.

Second, the state could look to expand the sales tax to services. A study the Illinois Commission on Government Forecasting and Accountability found that expanding the sales tax to services, while exempting business-to-business transactions (an essential step), could net Illinois $4 billion to state government and $1 billion to local government annually [4]. In addition to this, this state could look to expand the sales tax to currently exempted items like food and medical goods. Though we don’t recommend raising the sales tax rate, if at all possible, particularly given that it rates 10th currently, it’s worth noting that at a given level of state spending, it’s always preferable to raise revenue through consumption taxes versus income taxes. That said, we don’t recommend raising the sales tax unless it’s done in a revenue fashion, given that Illinois is already a high tax burden state and all taxes, however well structured, hurt economic growth.

What I would suggest Illinois avoid doing is attempting to lower the burden of personal and corporate income taxation through various credits, deductions, and cash incentives—tax carve-outs. Though these incentives may help lure one business or industry to the state, they don’t lead to the type of robust, widely shared, and sustainable growth Illinois should be aiming for. There is no way to know what industries and businesses will lead to future hiring and wage growth. Illinois should avoid picking winners and losers and instead, “open for business” to all individuals and firms. By exempting some people, firms, or industries from higher marginal rates, all the state does is raise the rate of taxation for all those who don’t qualify for the incentives. Even for firms that receive incentives, the threat of eventual phase-out or repeal of the credit is a disincentive to locating or growing in Illinois. Along these lines, Illinois would be well served by looking to eliminate current tax carve-out and incentives in the system in order to pay for rate reductions. Broad tax bases and low rates is just another way of saying sound tax policy.

At the very least, Illinois should consider more aggressively evaluating the economic performance of tax carve-outs and incentives. ALEC has recently passed model policy, modeled after policy passed in Washington state, that requires all tax carve-outs have an explicitly stated and measurable goal, annual reporting of the individual cost of every carve-out, and annual reporting of how well the carve-out is meeting its measurable goal [5]. I’m happy to share the text of this proposal with any legislators and answer questions about the proposal.

Though there is much additional research and policy recommendation I’d like to share with you, my time is quickly coming to a close. So at this time, I’ll conclude my remarks and welcome your questions, as well as follow-up conversation in the future. I’m willing to offer my assistance to any member of the Illinois legislature in any way I can. Thank you very much.

[1] See “Tax Myth Debunked” by Dr. Randall Pozdena and Dr. Eric Fruits, publish by the American Legislative Exchange Council: http://www.alec.org/publications/tax-myths-debunked/

[2] See “What’s the Evidence on Taxes and Growth” by Dr. William McBride, published by the Tax Foundation: http://taxfoundation.org/article/what-evidence-taxes-and-growth

[3] See “What’s the Evidence on Taxes and Growth” by Dr. William McBride, published by the Tax Foundation: http://taxfoundation.org/article/what-evidence-taxes-and-growth

[4] See “Service Taxes: 2011 Update” by the Illinois Commission on Government Forecasting & Accountability: http://cgfa.ilga.gov/upload/servicetaxes2011update.pdf

[5] See the “Tax Expenditure Transparency Act” by the American Legislative Exchange Council: http://www.alec.org/model-legislation/tax-expenditure-transparency-act/